- The Stacker Report: Your Source For Silver Market Insights

- Posts

- The “2020 Vibe” Is Back — And Markets Are Starting to Crack

The “2020 Vibe” Is Back — And Markets Are Starting to Crack

History Does Not Repeat, But It Often Rhymes

Smart Silver Stacker

March 29, 2026

There’s a familiar feeling creeping into the market right now—something that feels a lot like early 2020.

Not necessarily the same trigger, but the same underlying dynamic:

a growing disconnect between what’s being said and what’s actually happening beneath the surface.

While headlines still lean toward optimism, several key signals suggest the system is under increasing strain.

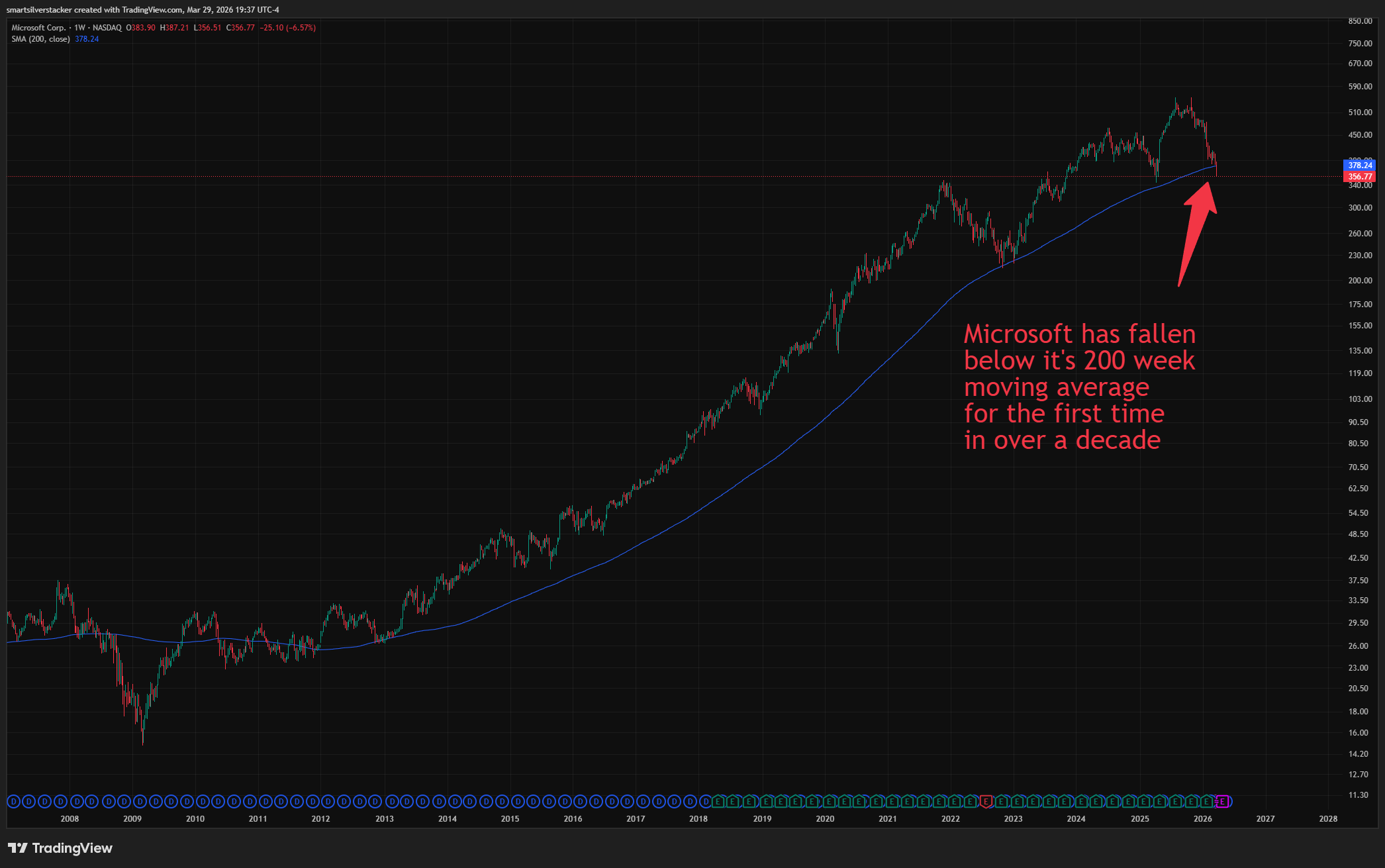

1. Cracks in Market Leadership

One of the more concerning developments is weakness in major tech names.

When large-cap leaders—especially names like Microsoft—start breaking long-term support levels (like the 200-week moving average), it raises a bigger question:

If the strongest companies are losing momentum, what does that say about the broader market?

Valuations are still elevated (Shiller P/E north of 36), which leaves very little room for error in an environment where liquidity is tightening.

2. Markets Are Ignoring the Narrative

We’re also seeing diminishing impact from political messaging.

Recent announcements around “peace talks” briefly moved markets—but the reaction was muted and quickly faded. Meanwhile, real-world developments (continued strikes, escalation risks) contradicted the narrative almost immediately.

Markets are starting to price reality over rhetoric.

That’s a shift worth paying attention to.

3. Oil Is the Pressure Point

Oil remains one of the most important variables right now.

Technically, crude appears to be forming a bullish structure (an ascending triangle), suggesting potential for further upside. But more importantly, the fundamental backdrop supports higher prices:

Ongoing geopolitical tensions

Supply disruptions

Tight global energy markets

Higher energy prices act like a tax on the global economy—and historically, they’ve been a major catalyst for recessions.

Beyond oil, there are early signs of strain in less visible but critical areas:

Helium shortages (important for semiconductor manufacturing)

Fertilizer constraints tied to natural gas

Agricultural input pressure feeding into food inflation

These aren’t headline-grabbing issues yet—but they tend to show up later in the form of higher costs and slower growth.

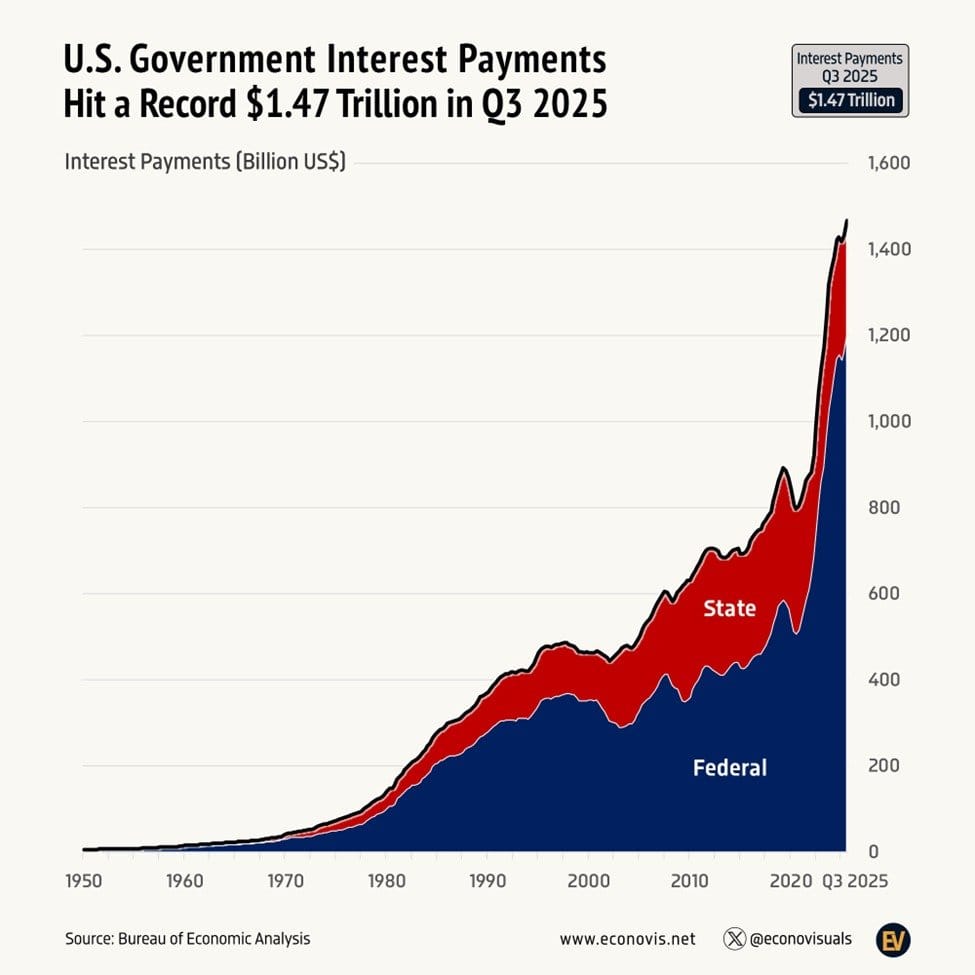

5. The Debt Problem Isn’t Going Away

At the same time, the U.S. is dealing with structurally high debt levels and rising interest costs.

As yields move higher, the cost to service that debt increases—creating a feedback loop:

Higher rates → higher debt servicing costs → more pressure to ease policy

This tension between inflation and debt sustainability is one of the defining forces in markets right now.

Soaring debt service cost make the Fed’s inflation fight much more challenging

6. Metals: Correction, Then a Shift

Gold and silver have gone through a meaningful correction over the past couple of weeks, largely in line with a stronger dollar and rising oil—both of which had been pressuring prices.

But Friday was different.

We saw the DXY and oil move higher again, yet metals rallied instead. That’s a subtle shift, and something I’m watching closely.

That said, I still think metals are vulnerable in the event of a broad market sell-off. If we get that kind of risk-off move, they could see an initial knee-jerk drop along with everything else.

In my view, that would likely be a buying opportunity ahead of the next phase—where the Fed is forced to step in, liquidity returns, and the inflationary backdrop reasserts itself.

Final Thought

We’re not necessarily in a crisis yet—but the ingredients are there:

Geopolitical instability

Rising energy prices

Tightening liquidity

Structural debt issues

Markets can ignore these things… until they can’t.

The key question going forward:

Are you positioned for stability—or for volatility?

Stay Safe & Happy Stacking,

Smart Silver Stacker

PS: For more in depth coverage on these topics, check out my most recent YouTube Livestream: https://youtube.com/live/ZkzZ5n0X4U8

Disclaimer

This content is for informational and educational purposes only and should not be considered financial advice. I am not a financial advisor. All opinions expressed are my own and are based on publicly available information and personal interpretation of market conditions. Always do your own research and consult with a qualified professional before making any investment decisions.