- The Stacker Report: Your Source For Silver Market Insights

- Posts

- The Brink of Calamity: Navigating the Geopolitical and Debt-Driven Economic Crisis

The Brink of Calamity: Navigating the Geopolitical and Debt-Driven Economic Crisis

Smart Silver Stacker

March 24, 2026

The current disconnect between official diplomatic narratives and the reality on the ground in the Middle East suggests that messaging itself has become a tool for market stabilization. The President’s recent social media posts—released just ahead of the market open Monday Morning —highlighted “productive conversations” with Iran. Yet those claims were quickly dismissed by Iranian officials, raising questions about whether this was less about diplomacy and more about managing market sentiment in a fragile moment.

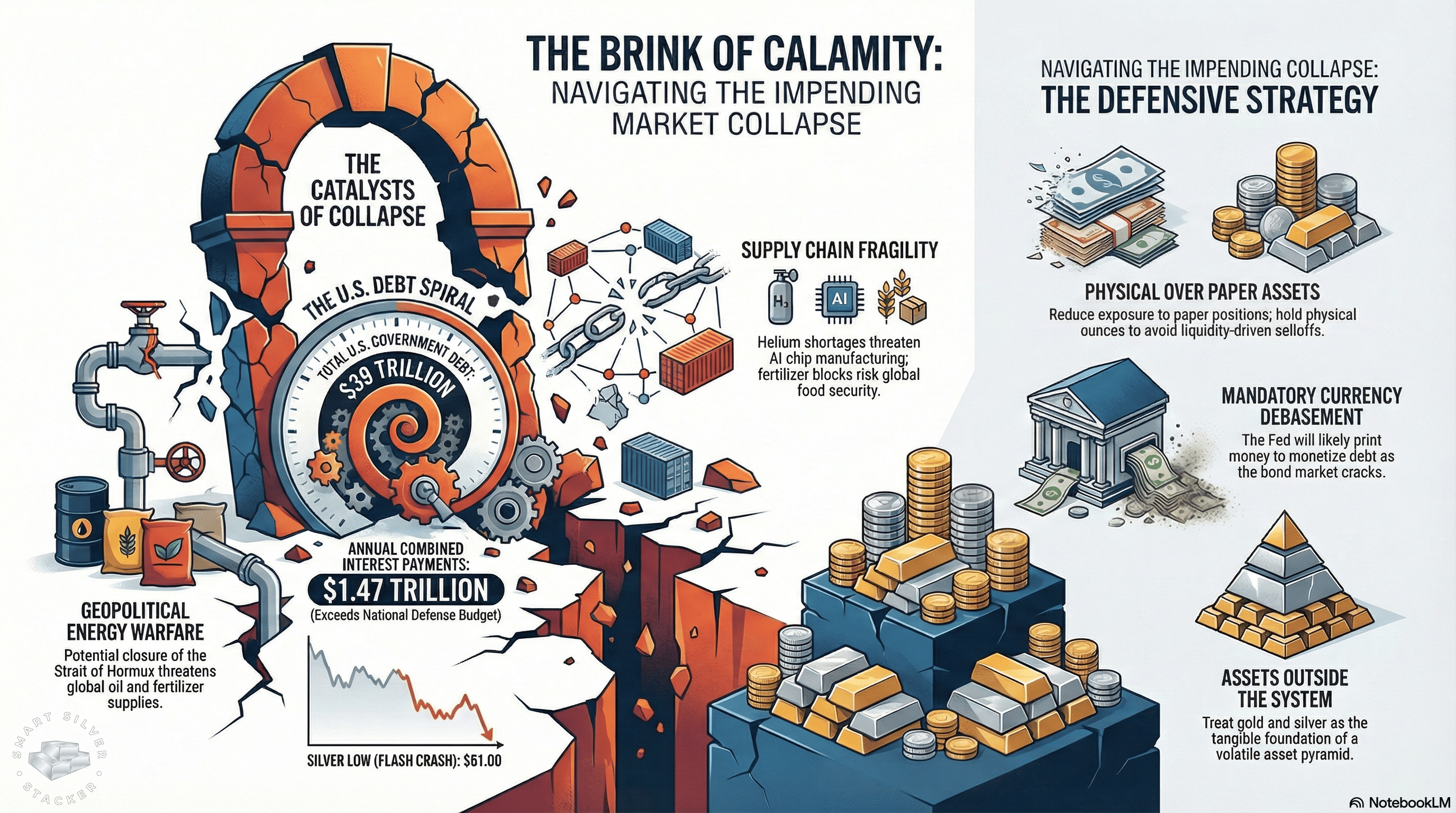

At the same time, the underlying situation has not materially improved. Energy infrastructure remains under pressure. Strikes on Iranian gas facilities, the Port Arthur refinery fire—impacting roughly 400,000 barrels per day—and disruptions at Russia’s Primorsk export terminal all point to continued tightness in global energy markets. The idea that the Strait of Hormuz risk has been resolved may be premature. If anything, the situation appears to be temporarily de-escalated rather than structurally stable.

The more immediate and systemic issue, however, is the cost of debt.

As the 10-year U.S. Treasury yield continues to push higher, the implications for a nation carrying approximately $39 trillion in debt become increasingly serious. Recent data suggests that combined federal and state interest payments have reached roughly $1.4–$1.5 trillion annually, now rivaling or exceeding major budget categories like defense and Medicare.

This is where things start to matter.

At these levels, rising yields are no longer just a macro talking point—they directly threaten the sustainability of the system. The logical endgame is some form of Federal Reserve intervention. Whether that comes in the form of rate suppression, liquidity injections, or outright monetization, the path forward increasingly points toward a policy pivot. The alternative—a disorderly adjustment in the Treasury market—is something policymakers are unlikely to tolerate.

We’re also starting to see early signs of stress in less visible parts of the financial system.

Several large private credit firms—including Blue Owl, Ares Management, and Apollo—have recently moved to limit or halt investor redemptions. That doesn’t mean a full-blown crisis is here yet, but it does suggest that liquidity is tightening beneath the surface.

At the same time, geopolitical tensions are bleeding into the financial system in more subtle ways. There is growing rhetoric around the weaponization of capital flows and financial infrastructure, alongside ongoing supply chain disruptions—from energy to critical industrial inputs. None of these issues exist in isolation. Taken together, they point toward a more fragile and interconnected risk environment than markets may currently be pricing in.

For precious metals investors, the key distinction right now is between paper market volatility and physical fundamentals.

In a headline-driven environment like this, technical levels can be temporarily overridden—but they still provide useful context. Silver has recently tested its 200-day exponential moving average near the low $60s, while gold appears to be establishing support in the ~$4,000 range.

The main takeaway is this: volatility should be expected.

Short-term selloffs—especially those driven by liquidity events—are not necessarily bearish for the long-term thesis. In many cases, they may present opportunities. Maintaining liquidity, or “keeping powder dry,” allows you to take advantage of those moments rather than being forced to react to them.

In an environment where financial systems are under increasing strain, holding tangible assets outside that system is becoming less of a preference and more of a strategic consideration.

Looking ahead, the broader trajectory still points toward a familiar outcome.

If financial conditions tighten further—whether through rising yields, credit stress, or geopolitical escalation—the Federal Reserve will likely be forced to respond. While official policy may not yet reflect it, there are already signs of balance sheet expansion beneath the surface. If pressures continue to build, that response could accelerate significantly.

This is where the long-term framework comes into play.

Exter’s Pyramid provides a useful lens: as confidence erodes in higher layers of the financial system—debt, derivatives, and leverage—capital tends to migrate downward toward more fundamental forms of money. Historically, that has meant gold. Increasingly, it also includes silver.

That doesn’t mean a straight line higher. It does mean that the underlying drivers remain intact.

For investors who can navigate the volatility, the current environment is less about avoiding risk entirely—and more about understanding where that risk is being transferred.

If you want the full breakdown—including the charts, real-time reactions, and how I’m personally positioning around this—watch today’s livestream here:

👉 https://youtube.com/live/hQ5vOazo0RI

This is one of those moments where headlines are driving price action… but the bigger story is what’s happening underneath.

And that’s where the real opportunity is.

Stay Safe And Happy Stacking

-Smart Silver Stacker

Disclaimer: This content is for informational and educational purposes only and should not be considered financial advice. I am not a financial advisor. Always do your own research and consult with a qualified professional before making any investment decisions.